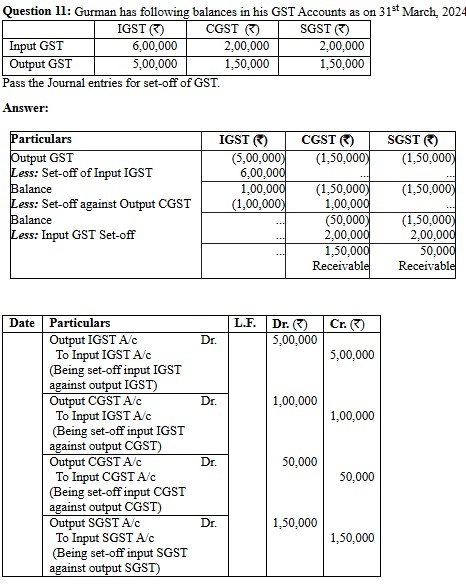

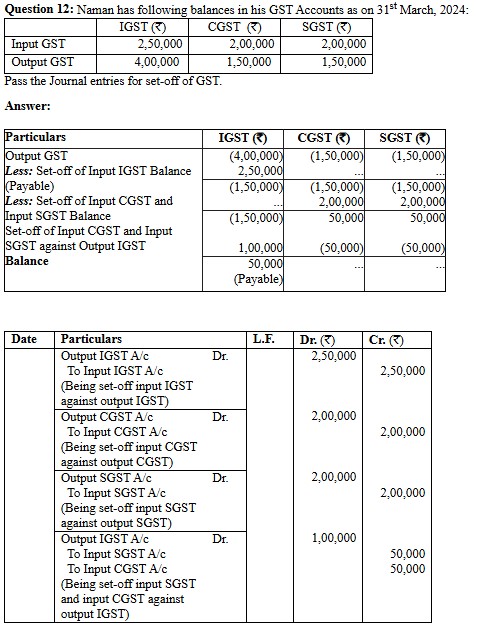

11th | Accounting for Goods and services (GST) | Question No. 11 And 12 | Ts Grewal Solution 2025-2026 by Click below for more QuestionsTs Grewal Solution 2025-2026Class 11th Chapter 12 – Accounting of Goods and Services Tax (GST)Question No. 1 and 2Question No. 3 and 4Question No. 5 and 6Question No. 7 and 8Question No. 9 and 10Question No. 11 and 12